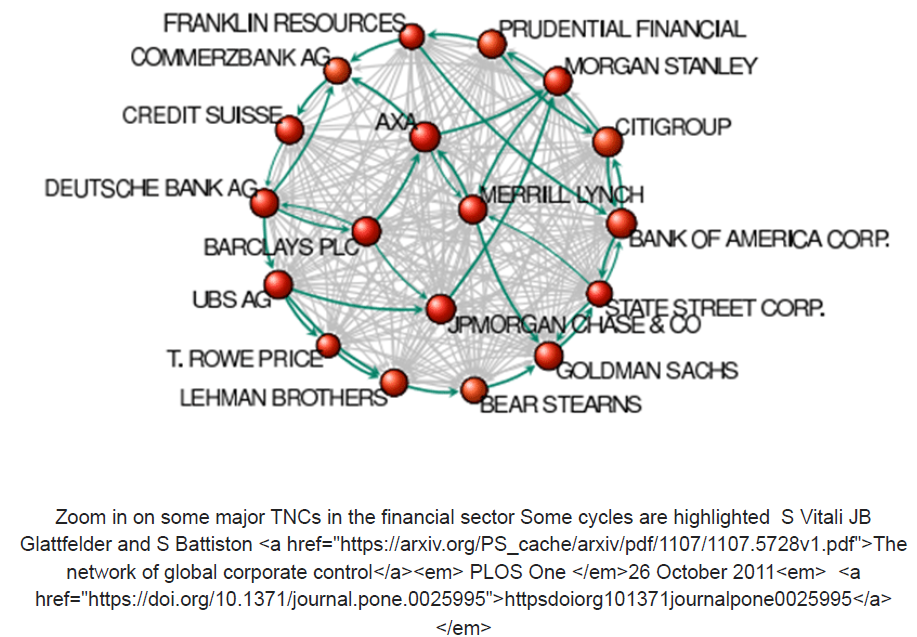

The structure of the control network of transnational corporations affects global market competition and financial stability. So far, only small national samples were studied and there was no appropriate methodology to assess control globally. We present the first investigation of the architecture of the international ownership network, along with the computation of the control held by each global player. We find that transnational corporations form a giant bow-tie structure and that a large portion of control flows to a small tightly-knit core of financial institutions. This core can be seen as an economic “super-entity” that raises new important issues both for researchers and policy makers.

Two issues are worth being addressed here. One may question the idea of putting together data of ownership across countries with diverse legal settings. However, previous empirical work shows that of all possible determinants affecting ownership relations in different countries (e.g., tax rules, level of corruption, institutional settings, etc.), only the level of investor protection is statistically relevant. In any case, it is remarkable that our results on concentration are robust with respect to three very different models used to infer control from ownership. The second issue concerns the control that financial institutions effectively exert. According to some theoretical arguments, in general, financial institutions do not invest in equity shares in order to exert control. However, there is also empirical evidence of the opposite [SI Appendix, Sec. 8.1]. Our results show that, globally, top holders are at least in the position to exert considerable control, either formally (e.g., voting in shareholder and board meetings) or via informal negotiations.